Euphoric reaction to superstar tech businesses is rampant — so much so that the tech industry is in denial about looming threats. The tech industry is in a bubble, and there are sufficient indicators for those willing to open their eyes. Rearing unicorns, however, is a distracting fascination.

The Perfect Storm

Raising funding for tech startups has never been so easy. Some of this flood of money has been because of mutual funds and hedge funds, including Fidelity, T. Rowe Price and Tiger Global Management. This is altering not only the funding landscape for tech startups, but also valuation expectations.

There are many concerns that valuations for businesses are confounding rationale. Entrepreneurs and their investors are deviating from more traditional valuation and performance metrics to more unconventional ones. Another cause cited for increasing valuations is the trend of protections for late investors that cause valuations to inflate further. The combination of a number of these factors has put the sector into a state of artificial valuations.

Meanwhile, the companies themselves are burning through cash like there is no tomorrow. Throwing money at marketing, overheads and, in particular, remuneration has become the accepted investment strategy for startup growth. All this does is perpetuate the vicious cycle of raising more money and spending more money. For the amounts that some of these businesses have raised, the jury is still out on actual profitability.

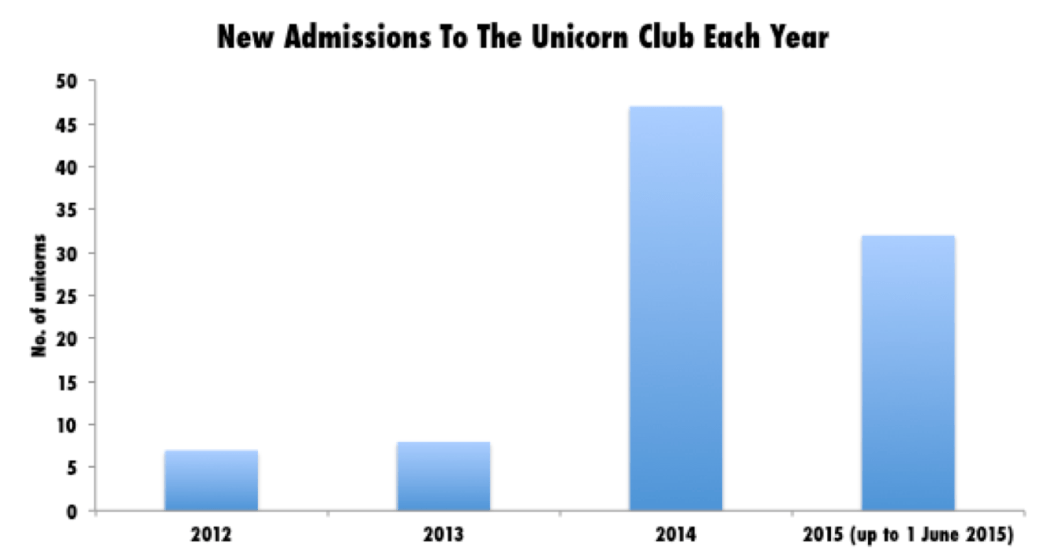

Unicorn Season

CB Insights publishes information on unicorns (companies with a valuation above $1 billion), which shows that access to the club has become increasingly less exclusive in the last couple of years. The chart below shows that the number of companies valued at $1 billion or above in 2014 exceeded previous years by quite some margin (47 unicorns joined the club in 2014 vs. 7 and 8 in 2012 and 2013, respectively). In addition, for the first 5 months of 2015, this trend shows no signs of abating (32 new unicorns as of June 1, 2015).

Different Experts, Same Conclusion

In the face of these trends, a small group of well-respected and influential individuals are voicing their concern. They are reflecting on what happened in the last dot-com bust and identifying fallacies in the current unsustainable modus operandi. These relatively lonely voices are difficult to ignore. They include established successful entrepreneurs, respected VC and hedge fund investors, economists and CEOs who are riding their very own unicorns.

Mark Cuban is scathing in his personal blog, arguing that this tech bubble is worse than that of 2000, because, he states, that unlike in 2000, this time the “bubble comes from private investors,” including angel investors and crowd funders. The problem for these investors is there is no liquidity in their investments, and we’re currently in a market with “no valuations and no liquidity.” He was one of the fortunate ones who exited his company, Broadcast.com, just before the 2000 boom, netting $5 billion. But he saw others around him not so lucky then, and fears the same this time around.

A number of high-profile investors have come out and said what their peers all secretly must know. Responding to concerns raised by Bill Gurley (Benchmark Capital) and Fred Wilson (Union Square Ventures), Marc Andreessen of Andreessen Horowitz expressed his thoughts in an 18-tweet tirade. Andreessen agrees with Gurley and Wilson in that high cash burn in startups is the cause of spiralling valuations and underperformance; the availability of capital is hampering common sense.

Read More

Comments

Post a Comment